- Mainland China’s central bank, regulators, and other ministries issued a notice about the ongoing ban on trading and mining Bitcoin and other crypto assets.

- The latest announcement also covered restrictions on entities engaging in crypto-related businesses.

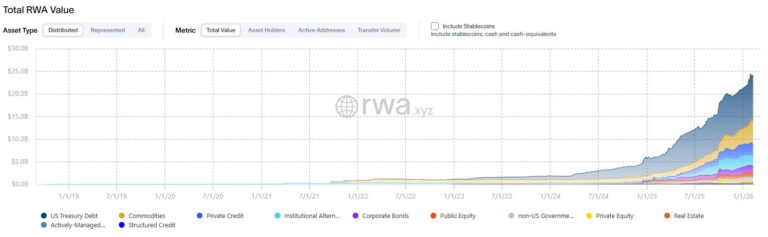

- The Chinese government likewise imposed a tight leash on RWA tokenization.

- The country listed stablecoins under “illegal financing activity” in light of the recent launch of the digital yuan CBDC.

The People’s Bank of China, the China Securities Regulatory Commission (CSRC), and six other government ministries have issued a notice reminding residents and businesses in mainland China of the ongoing ban on Bitcoin (BTC) and other cryptocurrency transactions. The document titled “Notice on Further Preventing and Handling Risks Related to Virtual Currencies” also covered restrictions on real-world asset (RWA) tokenization, including a stablecoin prohibition.

Reteiterating the Bitcoin and Crypto Trading, Mining, and Business Ban

According to a direct translation of the document on Google, the Chinese government reiterated the exact reasons why it imposed a ban on Bitcoin and other forms of crypto trading and mining in May 2021. It stated that such activities disrupt economic and financial order. Additionally, they are not recognized as legal tender and can endanger people’s properties.

The government extended the prohibition to businesses related to virtual currencies. It considered their operations as “illegal financing activity.”

Strict RWA Tokenization Controls and Restrictions

The latest announcement acknowledged the growing trend of RWA tokenization. Nonetheless, it viewed it as a breeding ground for “new challenges and situations for risk prevention and control.”

The government enacted a sweeping ban on RWA tokenization, except for “activities conducted based on specific financial infrastructure” with the approval of “competent business authorities,” in line with China’s laws and regulations.

The move comes after mainland China’s regulators reportedly asked Hong Kong, the country’s Special Administrative Region (SAR), to temporarily halt its RWA tokenization initiatives in September 2025. Sources claimed the CSRC warned the SAR’s Securities and Futures Commission (SFC) to strengthen its risk controls around them and ensure they operate in harmony with mainland laws.

The notice, however, explicitly restricted foreign individuals and entities from providing RWA tokenization-related services to domestic entities in any form. Moreover, the government enforced a non-negotiable ban on stablecoins, underscoring the fact that they are not legal tender and that their use constitutes “illegal financing activity.”

The new measures come hot on the heels of China’s launch of its yield-bearing digital yuan (e-CNY) Central Bank Digital Currency (CBDC).

Holding Bitcoin and Other Crypto Assets

The notice said the new rules override the previous provisions that banned Bitcoin and crypto trading and mining, as well as the operation of virtual currency-related businesses. But then again, it remained silent on whether merely holding or possessing them is also illegal.

Before the ban five years ago, the Shanghai High Court had classified Bitcoin as a virtual property. The judgment applied the same ruling it had for other virtual currencies and online game assets, which held that they enjoy an equal level of protection as physical property under China’s civil code.

The High Court of Hong Kong similarly handed a landmark decision in 2023 concerning crypto. It ruled in the Gatecoin case that, because property laws apply to digital assets, they can also be placed in a trust.

What’s your Reaction?

+1

0

+1

0

+1

0

+1

0

+1

0

+1

0

+1

0